Siguiente Riesgos dispersos y una crisis sin nombre, por Gonzalo Gómez Bengoechea

El primaveral –por la época, no por el símil poético– intercambio de declaraciones entre EE.UU. e Irán sobre acuerdos de paz, o no, y sobre cierres y bloqueos de Ormuz, o no, ha sido una constante montaña rusa de subidas y bajadas del precio del petróleo, principalmente, y de otras mercancías, que transitan hacia el destino final por el famoso paso entre Irán y Omán en su navegar por el Mar Arábigo. En el momento de escribir estas líneas, el precio de los barriles de referencia a uno y otro lado del Atlántico ha bajado en torno a un 40% con relación a los picos “registrados” durante los sucesivos recrudecimientos del conflicto. Tras cuatro meses de bloqueo, los precios siguen una tendencia a acercarse a los que se marcaban a mediados de febrero (los bombardeos a Irán y las consecuencias en Ormuz comenzaron el 28 de febrero).

LAS PRESIONES ESTÁN IMPULSANDO LA INFLACIÓN MUNDIAL, QUE PODRÍA AUMENTAR AL 4,0% ESTE AÑO. UN INCREMENTO SUSTANCIAL FRENTE AL 3,3% DE 2025” (GBM)

Perspectivas

Unos días antes del “acuerdo definitivo”, con los precios del crudo ya en franco descenso, el Grupo Banco Mundial (GBM) presentó su informe Global Economic Prospects, en el que explican cómo “el cierre del estrecho de Ormuz ha causado graves disrupciones en los mercados energéticos, por lo que se prevé que el petróleo crudo Brent alcance un precio promedio de 94 dólares por barril en 2026, un 36% por encima de los niveles de 2025, bajo el supuesto de que las peores perturbaciones se atenúen en julio. Se proyecta que los precios de los fertilizantes aumentarán considerablemente este año, lo que tendrá efectos indirectos en los precios de los alimentos. En conjunto, estas presiones están impulsando la inflación mundial, la que podría aumentar al 4,0% este año, un incremento sustancial frente al 3,3% de 2025”.

LAS NAVIERAS QUIEREN TENER GARANTÍAS DE QUE SUS BARCOS NO VAN A SER ATACADOS O A SUFRIR INCIDENCIAS Y DE QUE LAS ASEGURADORAS BAJARÁN SUS PRIMAS

Sin embargo, y dicho esto a expensas del largo devenir de vaivenes que cabe esperar durante los próximos meses con los “flecos” del alto el fuego, el Brent se situó en la “semana del anuncio” por debajo de 77 dólares. Seguramente, porque las expectativas del memorando señalan que se podría añadir rápidamente suministro al mercado internacional. Esto sucedería si Teherán reanuda toda su capacidad de exportación de petróleo inmediatamente y suaviza las restricciones impuestas al transporte en el estrecho de Ormuz. Por otro lado, las decenas de buques (en torno a un millar, según Windward, unos cuarenta de ellos superpetroleros, para Vortexa) cargados de crudo que están bloqueados en el Golfo Arábigo, una vez libres para atravesar el Estrecho, podrían incrementar el suministro (“Barcos del mundo: ¡arranquen motores! ¡Que fluya el petróleo!”, ya saben…). Con este panorama, quizás sea más oportuno tener en cuenta las previsiones de Goldman Sachs y JPMorgan, que pronostican un Brent en el rango de 56 a 65 dólares para todo 2026; es decir, bastante menos que las proyecciones del GBM.

TENDREMOS QUE CONFIAR EN QUE EL MERCADO SE REGULE CON LA CAÍDA DE DEMANDA COMO CONSECUENCIA DE LOS ALTOS PRECIOS (EL “EFECTO ACORDEÓN”)

Sin prisas

Dando por cierto que la tregua vaya a ser permanente, la recuperación de una situación similar a la que había a principios de 2026 va a tardar en llegar. Hablamos, por recordarlo, del 20% del petróleo y el 17% del gas natural licuado que se consume en el mundo. Por un lado, el renovado flujo de petróleo tiene que reponer las reservas que hemos ido utilizando para compensar el crudo que no llegaba a las destilerías. Recordemos que la Agencia Internacional de la Energía liberó en marzo, ante la situación, 400 millones de barriles de reservas estratégicas. Por otro, hay que ir pensando en el consumo ordinario, que suele ser más elevado en invierno. Hablamos como mínimo, pues, de los 14 millones de barriles día que circulaban antes del conflicto por Ormuz, más un posible aumento de producción por parte de la OPEP, que juega con un remanente de más de dos millones de barriles diarios para estabilizar los precios.

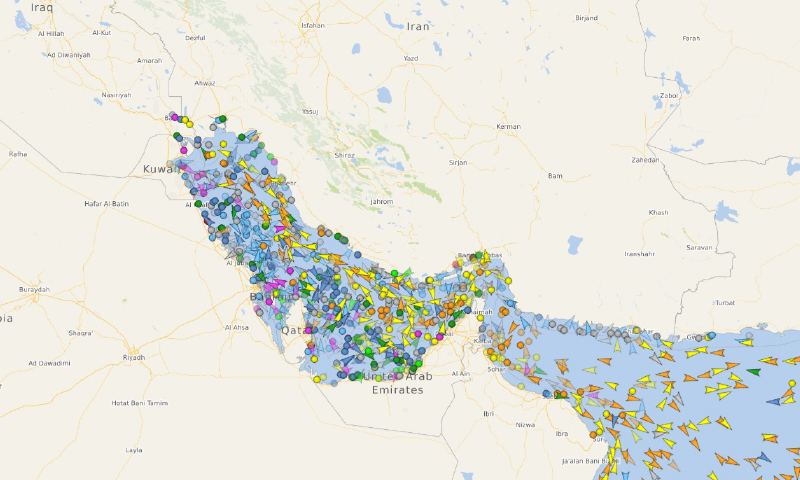

A partir de aquí entran en juego las navieras, que quieren tener garantías de que sus barcos no van a ser atacados o a sufrir incidencias por las acciones de cualquiera de los bandos; y seguridad de que se ha procedido al total desminado del cuello de botella de poco más de treinta kilómetros en el que ahora se centran los problemas. Como dato, la Organización Marítima Internacional (OMI, organismo dependiente de la ONU), en una declaración del 11 de junio, ha manifestado que se produjeron 46 ataques contra cargueros en el Estrecho desde el inicio de la contienda, con catorce víctimas mortales entre la marinería. En este contexto económico hay que añadir a las aseguradoras, que han incrementado en un 300% sus primas para los petroleros que hacen la ruta de Ormuz, lo que supone un sobrecoste en torno al 30% en el precio del barril, sea cual sea la oferta de crudo de que disponen el mercado. En resumen, esa normalidad a la que antes nos referíamos llegará, si no cambia la situación respecto junio de 2026, en los primeros meses de 2027.

A partir de aquí entran en juego las navieras, que quieren tener garantías de que sus barcos no van a ser atacados o a sufrir incidencias por las acciones de cualquiera de los bandos; y seguridad de que se ha procedido al total desminado del cuello de botella de poco más de treinta kilómetros en el que ahora se centran los problemas. Como dato, la Organización Marítima Internacional (OMI, organismo dependiente de la ONU), en una declaración del 11 de junio, ha manifestado que se produjeron 46 ataques contra cargueros en el Estrecho desde el inicio de la contienda, con catorce víctimas mortales entre la marinería. En este contexto económico hay que añadir a las aseguradoras, que han incrementado en un 300% sus primas para los petroleros que hacen la ruta de Ormuz, lo que supone un sobrecoste en torno al 30% en el precio del barril, sea cual sea la oferta de crudo de que disponen el mercado. En resumen, esa normalidad a la que antes nos referíamos llegará, si no cambia la situación respecto junio de 2026, en los primeros meses de 2027.

A PESAR DE LOS “PICOS DE SIERRA” DE LA ENERGÍA, LOS PRINCIPALES ÍNDICES BURSÁTILES DEL MUNDO HAN SEGUIDO CRECIENDO EN LO QUE LLEVAMOS DE 2026

Escenarios

Dado que en Escritura Pública no tenemos “bola de cristal”, encomendamos al lector el cálculo de probabilidades económico-financieras según se vaya moviendo ese damero maldito en el que nos ha metido a todos la insensatez, como mínimo, más palmaria. Unos apuntes: si la cosa vuelve a ponerse muy fea, lo que parece poco probable, nos enfrentaríamos una preocupante recesión en Europa y Asía; si el “acuerdo” normaliza la situación previa al enfrentamiento armado, las aseguradoras bajarán precios, se reequilibrará el precio del Barril y crecerá la producción, al menos hasta que se repongan las reservas; y, como escenario con más probabilidades, que la paz no se consolide en primera instancia, de manera que cada fleco a consensuar se convierta en un abro/cierro Ormuz, en el mejor de los casos (en el peor, nuevos vuelos de misiles y drones), con lo que tendremos que confiar en que el mercado se regule con la caída de demanda como consecuencia de los altos precios (el “efecto acordeón”: combustible más caro, subida de la inflación, caída de la demanda).

SI SE BLOQUEA LA ENTRADA Y SALIDA DE MERCANCÍAS EN TAIWÁN, DEJARÍA DE EXPORTARSE MÁS DE UN 90% DE LOS SEMICONDUCTORES UTILIZADOS POR TODAS LA TECNOLÓGICAS DEL MUNDO

En esa mención al cuento de pastores y lobos, en nuestra entradilla, decíamos que los seres humanos nos acabamos acostumbrando a las “bromas”, en este caso un tanto macabras por la pérdida de vidas humanas directas, la destrucción de “calidad de vida” y mayores problemas para los países más débiles, e intentando que otras cosas compensen las dificultades. Por ejemplo, y a pesar de los “picos de sierra” de la energía, los principales índices bursátiles del mundo han seguido creciendo en lo que llevamos de 2026. Es verdad que no del todo ajenos a los vaivenes del crudo; por ejemplo, el KOSPI de Corea del Sur dio un subidón cuando parecía que el “acuerdo” era, de verdad de la buena, inminente, porque sus tecnológicas (las que “tiran del carro”) dependen del transporte y éste, del combustible. Es, precisamente, todo lo que se relaciona con las industrias tecnológicas lo que está aportando ese equilibrio que la normalidad financiera precisa. Ahí están las grandes inversiones en centros de datos que precisa la inteligencia artificial, la propia AI y los componentes necesarios para que evolucione, las grandes salidas a bolsa, como ya la efectiva del SpaceX de Elon Musk o las previstas de Anthropic y OpenAI, o los movimientos financieros de Google, Amazon o Meta. Y aquí se puede quedar una pregunta en el aire: ¿todo ese capital que va a parar a las tecnológicas no habrá salido, en gran medida, de las ganancias de las energéticas como consecuencia del conflicto? Solo un dato: según Oxfan Intermon, cuarenta y un milmillonarios de la energía de los países del G7 (Alemania, Canadá, Francia, Italia, Japón y el Reino Unido) han aumentado su riqueza en 23.500 millones de dólares desde que comenzó el conflicto armado entre EE.UU., Israel e Irán.

Temores

Si el bloqueo de un paso marítimo como Ormuz nos tiene un tanto alterados, imagine el lector la que se pude venir encima si lo que se obstaculiza es la producción y la exportación de semiconductores de Taiwán. Como de costumbre, un dato: la compañía Taiwan Semiconductor Manufacturing Company Limited (TSMC) fabrica la práctica totalidad de los semiconductores avanzados del mundo para empresas como como AMD, Apple, Marvell, Qualcomm o Nvidia. Y otro dato, al que no parece hayamos dado mucha importancia, como ciertas declaraciones del mandatario chino Xi Jinping, diciendo a sus militares que deberían de estar preparados para el momento en que fuera posible lograr la “ansiada reunificación” con la isla. Si simplemente se desata un tira y afloja y se bloquea la entrada y salida de mercancías en Taiwán, dejaría de exportarse más de un 90% de los semiconductores utilizados por todas la tecnológicas del mundo y a la isla dejarían de llegar productos energéticos y de alimentación (importa un 90% y un 60%, respectivamente, de su consumo). ¿El resultado? Una caída aproximada del 5% del producto interior bruto mundial.

Y, por poner un poco de humor negro, las posibles “burbujas”: la del hombre más rico del mundo, la de la IA, la de las criptomonedas… Ya hay quien pronostica “días de vino y rosas” si llegan a darse todas juntas. Pero sin un ápice de pesimismo, que conste.

Global Economic Prospects. World Banl Group (junio de 2026).

Global Economic Prospects. World Banl Group (junio de 2026).

Oil Market Report. Agencia Internacional de la Energía (junio de 2026).

Oil Market Report. Agencia Internacional de la Energía (junio de 2026).

Promesas y retos: ¿qué podría salir mal y qué podría salir bien? JP Morgan (perspectivas de mitad de año de 2026)

Promesas y retos: ¿qué podría salir mal y qué podría salir bien? JP Morgan (perspectivas de mitad de año de 2026)

The spring-like exchange of statements – referring to the season, not the poetic simile – between the U.S . and Iran regarding peace agreements – or the lack thereof – and the closure or unblocking of the Strait of Hormuz – or not – has been a constant rollercoaster of ups and downs, primarily in the price of oil, but also in other commodities, as they make their way to their final destination via the famous strait between Iran and Oman whilst sailing through the Arabian Sea. At the time of writing, the price of benchmark crude oil on both sides of the Atlantic has fallen by around 40% compared with the peaks “recorded” during the successive escalations of the conflict. After four months of the blockade, prices are continuing their trend towards the levels seen in mid-February (the air strikes on Iran and their impact on the Strait of Hormuz began on 28 February).

PRESSURES ARE DRIVING UP GLOBAL INFLATION, WHICH COULD RISE TO 4.0% THIS YEAR. «A SUBSTANTIAL INCREASE COMPARED WITH THE 3.3% FIGURE FOR 2025» (GBM)

Outlook

A few days before the “final agreement”, with crude oil prices already in sharp decline, the World Bank Group (WBG) presented its Global Economic Prospects report, in which it explains how “the closure of the Strait of Hormuz has caused serious disruptions in energy markets, and as a result, Brent crude oil is forecast to reach an average price of $94 per barrel in 2026, 36% above 2025 levels, assuming that the worst disruptions ease by July. Fertiliser prices are forecast to rise significantly this year, which will have knock-on effects on food prices. Taken together, these pressures are driving up global inflation, which could rise to 4.0% this year – a substantial increase on the 3.3% recorded in 2025.”

However, and having said that – whilst acknowledging the long period of volatility that is likely to unfold over the coming months as the “loose ends” of the ceasefire are sorted out – Brent crude stood below $77 during the “week of the announcement”. No doubt because the memorandum’s projections suggest that supply could be rapidly increased on the international market. This would happen if Tehran were to immediately resume its full oil export capacity and ease the restrictions imposed on shipping in the Strait of Hormuz. Meanwhile, the dozens of vessels (around a thousand, according to Windward; some forty of them supertankers, according to Vortexa) laden with crude oil that are currently stranded in the Arabian Gulf could, once free to pass through the Strait, boost supply (“Ships of the world: start your engines! “Let the oil flow!”, as you know…). Against this backdrop, it might be more appropriate to take into account the forecasts from Goldman Sachs and JPMorgan, which predict that Brent will trade in the range of $56 to $65 throughout 2026; that is, considerably lower than the GBM’s projections.

SHIPPING COMPANIES WANT ASSURANCES THAT THEIR VESSELS WILL NOT BE ATTACKED OR SUFFER INCIDENTS, AND THAT INSURERS WILL REDUCE THEIR PREMIUMS

No rush

Assuming that the truce is to be permanent, it will take some time for conditions to return to those that existed in early 2026. To recap, we are talking about 20% of the oil and 17% of the liquefied natural gas consumed worldwide. On the one hand, the renewed flow of oil needs to replenish the reserves we have been using to make up for the crude that was not reaching the refineries. Let us recall that, in response to the situation, the International Energy Agency released 400 million barrels from its strategic reserves in March. On the other hand, we need to start thinking about our day-to-day consumption, which is usually higher in winter. We are therefore talking, at the very least, about the 14 million barrels per day that were passing through the Strait of Hormuz before the conflict, plus a possible increase in production by OPEC, which is drawing on a surplus of more than two million barrels per day to stabilise prices.

WE WILL HAVE TO TRUST THAT THE MARKET WILL SELF-REGULATE AS DEMAND FALLS AS A RESULT OF HIGH PRICES (THE “ACCORDION EFFECT”)

This is where the shipping companies come into the picture; they want assurances that their ships will not be attacked or suffer incidents as a result of actions by either side; and assurance that the bottleneck – stretching just over thirty kilometres, where the problems are currently concentrated – has been completely cleared of mines. For the record, the International Maritime Organisation (IMO, a UN agency), in a statement issued on 11 June, reported that there had been 46 attacks on cargo ships in the Strait since the start of the conflict, resulting in fourteen fatalities amongst the crew. In this economic context, we must also take into account the insurance companies, which have increased their premiums by 300% for oil tankers travelling through the Strait of Hormuz, resulting in an additional cost of around 30% per barrel, regardless of the supply of crude oil available on the market. In short, the return to normality we referred to earlier will take place – provided the situation does not change between now and June 2026 – in the first few months of 2027.

DESPITE THE “ROLLERCOASTER” NATURE OF THE ENERGY MARKET, THE WORLD’S LEADING STOCK MARKET INDICES HAVE CONTINUED TO RISE SO FAR IN 2026

Scenarios

Given that we at Escritura Pública do not have a “crystal ball”, we leave it to the reader to calculate the economic and financial probabilities as that cursed chessboard – into which the most blatant folly, to say the least, has plunged us all – continues to shift. A few notes: if things get really bad again – which seems unlikely – we would face a worrying recession in Europe and Asia; if the “agreement” restores the situation to how it was before the armed conflict, insurers will lower their premiums, the price per barrel will stabilise and production will increase, at least until reserves are replenished; and, as the most likely scenario, peace will not be consolidated initially, so that every minor detail to be agreed upon will result in the Strait of Hormuz being opened and closed, at best (at worst, further missile and drone strikes), in which case we will have to trust that the market will regulate itself through a fall in demand resulting from high prices (the “accordion effect”: more expensive fuel, rising inflation, falling demand).

In that reference to the tale of shepherds and wolves in our introduction, we said that we humans eventually get used to “jokes”, which in this case are somewhat macabre given the direct loss of human life, the destruction of “quality of life” and the greater problems faced by the weakest countries, whilst trying to ensure that other factors compensate for these difficulties. For example, despite the “energy price spikes”, the world’s leading stock market indices have continued to rise so far in 2026. It is true that they are not entirely immune to the ups and downs of the oil market; for example, South Korea’s KOSPI surged when it looked as though the “deal” was, in fact, imminent, because its tech companies (the ones “driving the market”) depend on transport, and transport, in turn, depends on fuel. It is, in effect, everything to do with the technology sectors that is providing the balance required for financial stability. There are the major investments in data centres required by artificial intelligence, AI itself and the components needed for it to evolve; major IPOs, such as the one already completed by Elon Musk’s SpaceX or those planned by Anthropic and OpenAI; and the financial manoeuvres of Google, Amazon and Meta. And this raises a question: might not much of the capital flowing into tech companies have come, to a large extent, from the profits of energy companies as a result of the conflict? Just one statistic: according to Oxfam Intermon, forty-one energy billionaires from the G7 countries (Germany, Canada, France, Italy, Japan and the United Kingdom) have seen their wealth increase by 23,500 million dollars since the armed conflict between the U.S., Israel and Iran began.

IF THE IMPORT AND EXPORT OF GOODS WERE BLOCKED IN TAIWAN, MORE THAN 90% OF THE SEMICONDUCTORS USED BY ALL THE WORLD’S TECHNOLOGY COMPANIES WOULD CEASE TO BE EXPORTED

Fears

If the blockade of a maritime strait such as the Strait of Hormuz has us somewhat concerned, the reader can imagine what might be in store if it were the production and export of semiconductors from Taiwan that were being disrupted. As usual, here’s a fact: Taiwan Semiconductor Manufacturing Company Limited (TSMC) manufactures virtually all of the world’s advanced semiconductors for companies such as AMD, Apple, Marvell, Qualcomm and Nvidia. And another point, which we do not seem to have attached much importance to, is certain statements made by Chinese President Xi Jinping, telling his military that they should be prepared for the moment when it becomes possible to achieve the “long-awaited reunification” with the island. If a simple tug-of-war were to break out and the flow of goods in and out of Taiwan were to be blocked, more than 90% of the semiconductors used by all the world’s technology companies would cease to be exported, and energy and food products would no longer reach the island (it imports 90% and 60%, respectively, of its consumption). The result? An estimated 5% fall in global gross domestic product.

And, to add a touch of dark humour, the potential “bubbles”: that of the world’s richest man, that of AI, that of cryptocurrencies… There are already those predicting “days of wine and roses” if they were all to come together. But let it be clear that I’m not being the slightest bit pessimistic.

Global Economic Prospects. World Bank Group (June 2026).

Oil Market Report. International Energy Agency (June 2026).

Promises and challenges: what could go wrong, and what could go right? JP Morgan (mid-year outlook for 2026)